As we near the end of another year it is always wise to review your financial situation – especially after a year like 2020! Leading Edge has created a checklist to help you evaluate your progress, maximize opportunities, and set goals for 2021. Take this opportunity to do a quick financial self-assessment. Did you meet your financial goals? Did you pay off the debts that you hoped to? Did you keep within your budget? If not, commit to making those changes for the upcoming year.

As always, we are here to help. Please reach out if we can help answer any questions or concerns. Schedule your free consultation today, 865-240-2292

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this document will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 12/23/2020 and are subject to change at any time due to the changes in market or economic conditions.

Not even Hollywood writers could have created a story like we lived out in2020.In this video, Charlie Mattingly and one of Leading Edge’s newest advisors, Rob Eklund,discuss what this year has taught us, howtobetterprepare in the future,andthoughts about the markets and economy going forward.

Leading Edge financial advisor Rob Eklund, aFirst Officer for a major airlineand a retired Air Force Pilot, reviewwhat investors can learn from mission planning in the Air Force and airlines.For example, how can we be proactive instead of reactive? Many times, people may remark how pilots need quick reactions to be successful. As Rob and I know, ifyou arefrequentlyreacting as a pilot,it’s a good indication you did notplansufficiently.We believe it’s the same withinvesting and retirement planning.

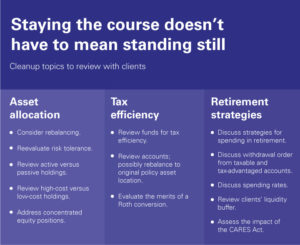

Although, it is to prepareprior to a recession or market downturn, there are many things we can do during the event itself. Vanguard posted the following graphic listingjust a few of the value-added strategies that are critical to consider during any market decline.

In addition to the checklist above from Vanguard, we believe there are ten essential principlesto help all of us remained focused and less stressed during the next market downturn or recession.

Embrace the efficiency of the markets in the long term.

In the short term,the stock marketreflects investor phycology (and many other unpredictable factors).However, over time, equity prices tend to represent the future cash flows of a business. We can all share in those future profits if we have the discipline to remain invested.

Don’t try to outguess the market.

Although there is some debate within the finance community on the exact level of impact on investment returns,most will agree that strategic asset allocation and the amount of time in the market (not market timing) have the most considerable influence on investor returns.

Resist chasing performance.

Do not select investments based on past returns. Funds that have outperformed in the past do not always persist as winners in the future. Past performance alone provides little insight into a mutual fund or ETFs ability to outperform in the future.

Let markets work for you.

The financial markets have historically rewarded long-term investors.We have the opportunity to earn an investment return that outpaces inflation by supplying capital to the companies we invest in. (I.e., stocks, mutual funds, exchange-traded funds)

Consider the drivers of returns.

Evidence shows that buying investments at a fair price (value factor), buying companies that demonstrate a consistent trend of profitability (profitability factor), and companies that tend to be smaller (small-cap premium)point to differences in expected future returns.

Practice smart diversification.

Diversification helps reduce risks that have no expected return. Global diversification can prove beneficial over the long term while reducing the short-term volatility of a portfolio.

Avoid market timing.

You never know which market segments will outperform from year to year. Time in the market is much more profitable than attempting to time the market.

Manage your emotions.

It’s challengingto differentiate the short-term ups and downs of the marketfromthe long-term returns needed to outpace inflation. In reality, themost significantrisk we face is losing purchasing powerover the long-term,during retirement, versus the risk of short-term losses in the market.

Look beyond the headlines.

There will ALWAYS be a news headline that could prevent you from investing in the stock market.The news headlines will either attempt to scare you out of the markets or lure you into the latest investing trend. Either strategy increases viewership,whichin turn sells more commercials.

Focus on what you can control.

As we mentioned at the beginning of the article, just like pilotsplan for their missions in greatdetail, we believe thorough planning is the best way to ensure a successfulinvesting experience plus a fulfilling and prosperous retirement.

Please don’t hesitate to call or email us anytime. We’d love to hear from you!

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 12/18/2020 and are subject to change at any time due to the changes in market or economic conditions.

As a brand-new pilot, one of the first things you learn is how to mitigate the risk of the potentially deadly physiological phenomenon known as spatial disorientation or spatial-D. In pilot speak, spatial-D is when your body is telling you one thing and your flight instruments (and airplane) are telling you something completely different. Sadly, spatial-D has claimed the lives of many pilots.

In this video, one of our newest Leading Edge team members and previous Marine F/A-18 fighter pilot, Mark Covell discusses just one example of spatial-D. Mark shares how carrier pilots tend to feel like they are pitching up as they are launched off the carrier at night due to the massive acceleration from the catapult. During daytime, VFR conditions this is probably a non-issue. However, in weather, or at night, this type of spatial-D is potentially deadly.

What does spatial-D have to do with investing and retirement planning? Personally, I feel like all of 2020 could be compared to being catapulted off a carrier at night and not knowing what is up or what is down.

During the heat of the battle from February until the markets settled a bit in early April, investor emotions were all over the place. Years of stock market gains evaporated in days, even hours. Furthermore, many people thought, and the news media quickly suggested we were headed for the second Great Depression. And don’t get me wrong, anything was (and is) possible. Sometimes, the unknown can be truly scary.

One slightly humorous example of investor spatial-D was early in the pandemic when the shares of ticker symbol ZOOM shot up due to investors buying up shares as quickly as possible. Zoom Technologies, a so-called penny stock had risen more than 240% in the span of a month before the SEC suspended trading. Unfortunately, the traders failed to realize the ticker symbol ZOOM did not represent the Cloud Video Conferencing company Zoom they thought they were purchasing – Ticker symbol ZM.

Here is the headline from MarketWatch.com dated February 27, 2020.

In the airplane, pilots must fight spatial-D by cross-checking and TRUSTING their instruments. If, as an investor, you did not trust your instruments during 2020, it may have been very costly.

So, it’s a dark night and the weather is terrible. What are the instruments you trust? What is your primary and backup instrument? Here are four instruments that I think can save your investments as well as your financial sanity during uncertain times…

1. Cash reserves – Emergency Funds.

Having extra cash can prevent withdrawals from retirement accounts or excessive credit card debt in emergencies. Studies also show having cash in a bank account makes people happy. In an article posted on PYMNTS.com, “Can Cash Really Make You Happier”, Joe Gladstone, research associate at the University of Cambridge in the U.K. and co-author of two recent studies about money and happiness said,

“We find a very interesting effect: that the amount of money you have in your bank account right now is a better predictor of happiness than your aggregate wealth,” Gladstone explained. “Having more money in their bank account makes people feel more financially secure, which leads to an increase in happiness.”

2. Have a working knowledge of financial history.

You don’t have to be an expert or financial historian, but I believe being familiar with financial history is akin to training before you go on a flying mission. Pilots call this chair flying. Athletes and musicians use a technique called visualization that helps them prepare for uncertainty and reduce anxiety for a sporting event or concert.

3. Admit that times are scary, and you do not know what’s going to happen.

This may sound silly, but I’ve seen many people get themselves into a “square corner” because they assumed that something was going to happen when in fact there was no indication or possible way of knowing what the future may hold. We have heard investors say “my gut tells me…” many times.

Some of the best investors in the world invest with the mindset of preparing to be wrong. That’s why diversification is not popular or “sexy” because it’s like admitting you don’t know what’s going to happen in the future, so you must prepare for multiple scenarios. However, diversification can feel disappointing but prove to be a profitable strategy over the long term.

BlackRock Investment Management Company posted the graphic below on their investor education website about diversification and “S&P Envy” over the last 20 years.

4. Prepare and Plan by having a clear vision of your goals and priorities.

If you don’t understand the “why” behind your investments as well as why you’re investing and saving in the first place, you will most likely bail-out of your plan during difficult and uncertain times. Changing your investment plan mid-crisis creates a very high likelihood that your investment returns will be significantly lower.

Simon Sinek started a movement by encouraging businesses to “Start with Why.” It’s a powerful mindset that leads to trust, inspiration and success. I believe the same applies to your financial and investment game plan.

5. Remember that you are invested in companies – not politics.

Sometimes our politics clouds the investment and retirement planning picture. This rule falls under the axiom; “control the controllable.” If you’re allowing your politics to affect your investment game plan than you may want to see rule number 2 above.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this video will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 12/09/2020 and are subject to change at any time due to the changes in market or economic conditions.